By Moe Ansari

You have bills to pay and a retirement to save for. Even if the thought of saving for your child’s education has crossed your mind, how can you make it happen amidst the never-ending financial pressures in life? It’s tempting to put saving for college on the back burner, but as anyone with kids knows, the days are long but the years are short. Regardless of whether your child is 2 or 12, you’ll be planning college visits and filling out applications before you know it.

Don’t get caught unaware and unprepared for college. Your child’s education is one of the most important investments you can make, and with today’s costs, it pays to plan ahead. As we approach National 529 College Savings Plan Awareness Day, it’s a good time to ask yourself this question: Have you started saving for your child’s future education costs? If not, here are 5 steps to get started.

1. Get The Facts

College tuition gets more expensive every year, and the numbers can cause anyone to break out in a sweat. Tuition rates have increased at a faster pace than many other expenses over the past decade, (1) and it doesn’t look like they will slow down anytime soon. In the past 10 years, college costs have risen an average of 1.86% a year for private schools and 2.2% for public colleges.

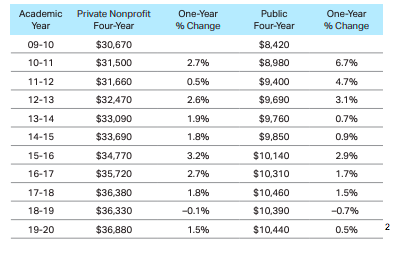

The following table shows the average cost for one year of tuition (not including other educational expenses):

Even though the drastic hikes tapered off recently, if the upward trend continues, in 25 years it could cost $300,000 to obtain a four-year undergraduate degree. The costs will vary depending on the institution attended, room and board, and other educational expenses, but either way, that’s a pretty penny for four years of school. For a 2019 graduate, the average student loan balance was $29,900 and the monthly student loan payment ranges between $200 and $299. (3) For students just beginning their careers, that’s a hefty bill to pay. The substantial cost may seem overwhelming, but knowing what to expect gives you a goal to aim for.

2. Hop On The Savings Train

It’s never too late or too early to start saving for your child’s college fund. By starting early, you can reap the rewards of compound interest. (4) If you wait, your account balance may not be as high, but you are still investing something toward your child’s future.

Even if you don’t think you have enough room in your budget to add another line item, $25 a month is still $25 more than $0. Setting up automatic contributions is a good way to remind yourself that college is getting closer, and your monthly account statement will keep this goal in the forefront of your mind. You can also make it a goal to save extra money from a raise or a bonus and invest it in your child’s future.

3. Decide How To Save

The most common method people use to save for college is through a 529 plan. A 529 plan is a state-sponsored education savings account that allows earnings to grow on a tax-deferred status. There are two categories of 529 plans: prepaid tuition plans and college savings plans.

Prepaid plans let you pay future tuition costs at today’s prices, which, considering skyrocketing college costs, can be enticing. On the other hand, college savings plans have no age or income restrictions and allow you to save anywhere from $235,000 to $529,000 per child, (5) and then use it, tax-free, for qualified education expenses. As an added benefit, you are not limited to using the plan offered by the state in which you live. Some states will give you a tax credit for using their plan, but in many cases, it’s worth it to shop around.

Beyond 529 plans, some families use Roth IRAs. Your Roth contributions can be withdrawn at any time and can be used for any purpose. In addition, Roth IRAs offer virtually unlimited investment options. Lastly, IRAs will not have any impact on your financial aid eligibility.

For college savings, Roth IRAs aren’t the perfect option, but they do offer an alternative to the traditional 529 plans. Think about opening a 529 plan for college but also continuing to contribute to a Roth for retirement. This strategy gives you extra resources to draw on if you need them.

4. Split It Up

While some people are able to save and pay for the total cost of their child’s college education, most people don’t fit into this category. Instead of letting that fact get you down, break the cost of college into thirds.

The first step is to save before your children head off to college. By starting early and having some help from the markets, you can accumulate a solid base to use for tuition as well as room and board. The next step is to plan on paying for about one-third of the costs while your child is in college. This can be through a combination of scholarships, grants, a part-time job for your child, or contributions from the family. The final piece is student loans that your child or you can repay after they have completed their education. Since the goal would be to minimize student loans, try to maximize the first two parts of this three-pronged strategy first.

5. Check Your Progress

Just like your 401(k) plan, you need to monitor your college planning investments. In the early days of saving for college, you will want to be more aggressive with your investments, but as college draws closer, the investment allocation should become more conservative, just like a retirement account. Some 529 plans even offer age-based investment options that automatically become more conservative as your child gets older. It is also helpful to monitor your balances, keep an eye on the changing college costs, and track your progress toward your goal.

If you need to get started saving for college, Compak Asset Management can help. We can explain all your 529 plan options and other strategies available to help you maximize the amount of money you have to send your child or grandchild to college. If you already have a 529 plan set up, it is important that you have an experienced professional managing the investments in your account to make sure you are still on track toward your goals.

With our guidance and expertise, you can start saving for your child’s future today so you can ease the worries of tomorrow. To get started, call 800-388-9700 or email investments@compak.com for a free consultation to get on the road to financial success!

The information in this discussion is current (and, we believe, accurate) as of the publication date but things can change. Be sure to talk with your financial and tax advisors about your own situation when making college savings investment decisions.

About Compak Asset Management

Compak Asset Management is an independent wealth manager providing custom-tailored portfolio and retirement solutions. Founded in 1999 by Moe Ansari, we are a fiduciary dedicated to providing clients with some of the best advice, ideas, and products to enhance their lives. Compak’s customized solutions and experienced team combine to deliver world-class wealth management and tailored financial plans to meet our clients’ financial needs. To learn more about Compak, please visit www.compak.com.

__________

(2) https://research.collegeboard.org/pdf/trends-college-pricing-2019-full-report.pdf

(3) https://studentloanhero.com/student-loan-debt-statistics/

(4) https://www.thebalance.com/the-power-of-compound-interest-358054